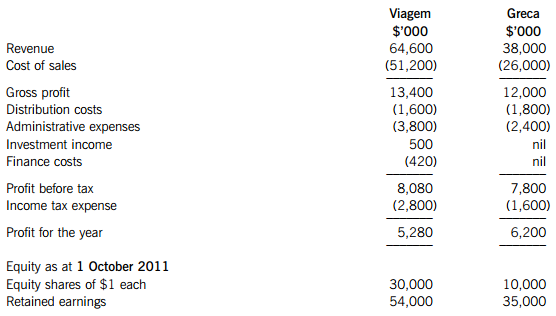

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

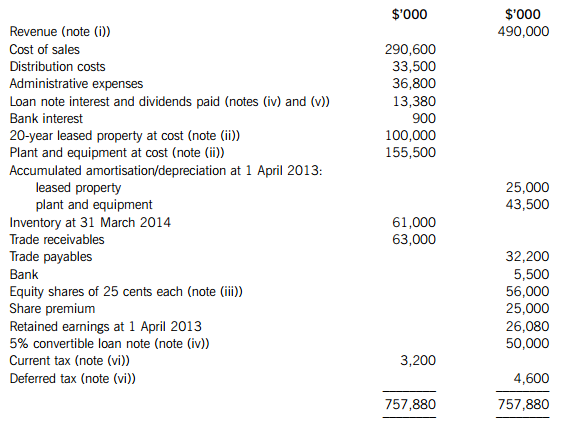

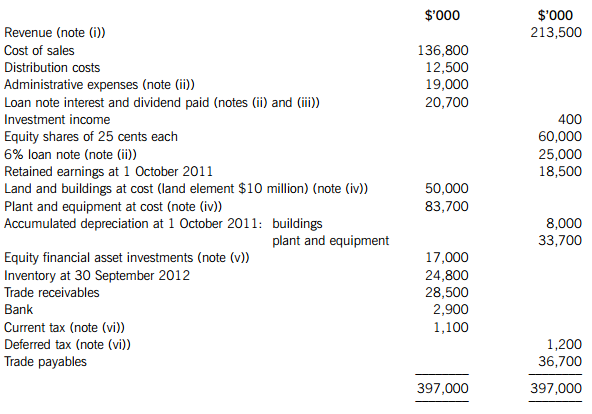

The following issues have arisen during the preparation of Skeptic’s draft financial state

(i) From 1 April 2013, the directors have decided to reclassify research and amortised development costs as administrative expenses rather than its previous classification as cost of sales. They believe that the previous treatment unfairly distorted the company’s gross profit margin.

(ii) Skeptic has two potential liabilities to assess. The first is an outstanding court case concerning a customer claiming damages for losses due to faulty components supplied by Skeptic. The second is the provision required for product warranty claims against 200,000 units of retail goods supplied with a one-year warranty.

The estimated outcomes of the two liabilities are:

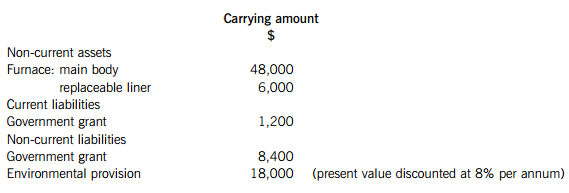

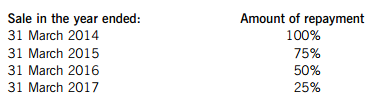

(iii) On 1 April 2013, Skeptic received a government grant of $8 million towards the purchase of new plant with a gross cost of $64 million. The plant has an estimated life of 10 years and is depreciated on a straight-line basis. One of the terms of the grant is that the sale of the plant before 31 March 2017 would trigger a repayment on a sliding scale as follows:

Accordingly, the directors propose to credit to the statement of profit or loss $2 million ($8 million x 25%) being the amount of the grant they believe has been earned in the year to 31 March 2014. Skeptic accounts for government grants as a separate item of deferred credit in its statement of financial position. Skeptic has no intention of selling the plant before the end of its economic life.

Required:

Advise, and quantify where possible, how the above items (i) to (iii) should be treated in Skeptic’s financial statements for the year ended 31 March 2014.

The following mark allocation is provided as guidance for this question:

(i) 3 marks

(ii) 4 marks

(iii) 3 marks

如搜索结果不匹配,请 联系老师 获取答案

如搜索结果不匹配,请 联系老师 获取答案