1 Thai Curry Ltd is a manufacturer of ready to cook food. The following information is ava

ilable in respect of the year

ended 30 September 2005:

Trading loss

The trading loss is £32,800. This figure is before taking account of capital allowances.

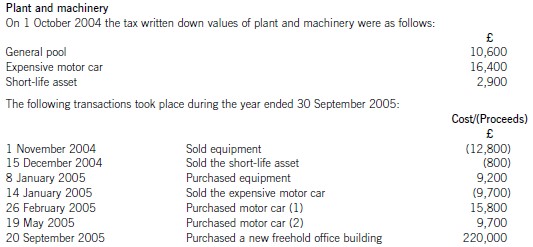

The equipment sold on 1 November 2004 for £12,800 originally cost £27,400. Motor car (2), purchased on

19 May 2005, is a low emission motor car (CO2 emission rate of less than 120 grams per kilometre).

The cost of the new freehold office building purchased on 20 September 2005 included £8,500 for the central

heating system, £7,200 for sprinkler equipment and the fire alarm system, £10,700 for the electrical and lighting

systems, and £7,050 for the ventilation system.

Thai Curry Ltd is a small company as defined by the Companies Acts.

Industrial building

On 1 October 2004 Thai Curry Ltd purchased a second-hand factory for £360,000 (excluding the cost of land). The

factory was originally constructed at a cost of £300,000 (excluding the cost of land), and was first brought into use

for industrial purposes on 1 October 1999. The factory was not used for industrial purposes during the period

1 October 2001 to 31 March 2003, but returned to industrial use from 1 April 2003 until the date of sale. The

previous owner of the factory prepared accounts to 31 March.

Income from property

Thai Curry Ltd lets out two warehouses that are surplus to requirements.

The first warehouse was let from 1 October 2004 until 31 May 2005 at a monthly rent of £2,200. On that date the

tenant left owing two months rent which Thai Curry Ltd was not able to recover. During August 2005 £8,800 was

spent on painting the warehouse. The warehouse was not re-let until 1 October 2005.

The second warehouse was empty from 1 October 2004 until 31 January 2005, but was let from 1 February 2005.

On that date Thai Curry Ltd received a premium of £60,000 for the grant of a four-year lease, and the annual rent of

£18,000 which is payable in advance.

Loan interest received

Loan interest of £8,000 was received on 30 June 2005, and £3,500 was accrued at 30 September 2005. The loan

was made for non-trading purposes.

Dividends received

During the year ended 30 September 2005 Thai Curry Ltd received dividends of £36,000 from African Spice plc, an

unconnected UK company. This figure was the actual cash amount received.

Profit on disposal of shares

On 28 July 2005 Thai Curry Ltd sold 10,000 £1 ordinary shares in African Spice plc, making a capital gain of

£155,300 on the disposal.

Other information

Thai Curry Ltd has three associated companies.

Required:

(a) Calculate Thai Curry Ltd’s tax adjusted trading loss for the year ended 30 September 2005. You should

assume that the company claims the maximum available capital allowances. (14 marks)

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

如搜索结果不匹配,请 联系老师 获取答案

如搜索结果不匹配,请 联系老师 获取答案

emission rate of 110 grams per kilometre. This motor car is used as a pool car by the company’s employees. The second motor car cost £13,200, and has a

emission rate of 110 grams per kilometre. This motor car is used as a pool car by the company’s employees. The second motor car cost £13,200, and has a