题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

Section A – BOTH questions are compulsory and MUST be attemptedNente Co, an unlisted compa

Section A – BOTH questions are compulsory and MUST be attempted

Nente Co, an unlisted company, designs and develops tools and parts for specialist machinery. The company was formed four years ago by three friends, who own 20% of the equity capital in total, and a consortium of five business angel organisations, who own the remaining 80%, in roughly equal proportions. Nente Co also has a large amount of debt finance in the form. of variable rate loans. Initially the amount of annual interest payable on these loans was low and allowed Nente Co to invest internally generated funds to expand its business. Recently though, due to a rapid increase in interest rates, there has been limited scope for future expansion and no new product development.

The Board of Directors, consisting of the three friends and a representative from each business angel organisation, met recently to discuss how to secure the company’s future prospects. Two proposals were put forward, as follows:

Proposal 1

To accept a takeover offer from Mije Co, a listed company, which develops and manufactures specialist machinery tools and parts. The takeover offer is for $2·95 cash per share or a share-for-share exchange where two Mije Co shares would be offered for three Nente Co shares. Mije Co would need to get the final approval from its shareholders if either offer is accepted;

Proposal 2

To pursue an opportunity to develop a small prototype product that just breaks even financially, but gives the company exclusive rights to produce a follow-on product within two years.

The meeting concluded without agreement on which proposal to pursue.

After the meeting, Mije Co was consulted about the exclusive rights. Mije Co’s directors indicated that they had not considered the rights in their computations and were willing to continue with the takeover offer on the same terms without them.

Currently, Mije Co has 10 million shares in issue and these are trading for $4·80 each. Mije Co’s price to earnings (P/E) ratio is 15. It has sufficient cash to pay for Nente Co’s equity and a substantial proportion of its debt, and believes that this will enable Nente Co to operate on a P/E level of 15 as well. In addition to this, Mije Co believes that it can find cost-based synergies of $150,000 after tax per year for the foreseeable future. Mije Co’s current profit after tax is $3,200,000.

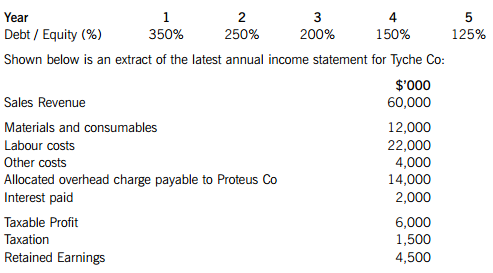

The following financial information relates to Nente Co and to the development of the new product.

Nente Co financial information

Extract from the most recent income statement

In arriving at the profit after tax amount, Nente Co deducted tax allowable depreciation and other non-cash expenses totalling $1,206,000. It requires an annual cash investment of $1,010,000 in non-current assets and working capital to continue its operations.

Nente Co’s profits before interest and tax in its first year of operation were $970,000 and have been growing steadily in each of the following three years, to their current level. Nente Co’s cash flows grew at the same rate as well, but it is likely that this growth rate will reduce to 25% of the original rate for the foreseeable future.

Nente Co currently pays interest of 7% per year on its loans, which is 380 basis points over the government base rate, and corporation tax of 20% on profits after interest. It is estimated that an overall cost of capital of 11% is reasonable compensation for the risk undertaken on an investment of this nature.

New product development (Proposal 2)

Developing the new follow-on product will require an investment of $2,500,000 initially. The total expected cash flows and present values of the product over its five-year life, with a volatility of 42% standard deviation, are as follows:

Required:

Prepare a report for the Board of Directors of Nente Co that:

(i) Estimates the current value of a Nente Co share, using the free cash flow to firm methodology; (7 marks)

(ii) Estimates the percentage gain in value to a Nente Co share and a Mije Co share under each payment offer; (8 marks)

(iii) Estimates the percentage gain in the value of the follow-on product to a Nente Co share, based on its cash flows and on the assumption that the production can be delayed following acquisition of the exclusive rights of production; (8 marks)

(iv) Discusses the likely reaction of Nente Co and Mije Co shareholders to the takeover offer, including the assumptions made in the estimates above and how the follow-on product’s value can be utilised by Nente Co. (8 marks)

Professional marks will be awarded in question 1 for the presentation, structure and clarity of the answer. (4 marks)

如搜索结果不匹配,请 联系老师 获取答案

如搜索结果不匹配,请 联系老师 获取答案