题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[主观题]

Je suis retourné dans le magasin pour acheter le joli meuble que je () _________________.

如搜索结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

如搜索结果不匹配,请 联系老师 获取答案

如搜索结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

如搜索结果不匹配,请 联系老师 获取答案

更多“Je suis retourné dans le magas…”相关的问题

更多“Je suis retourné dans le magas…”相关的问题

第2题

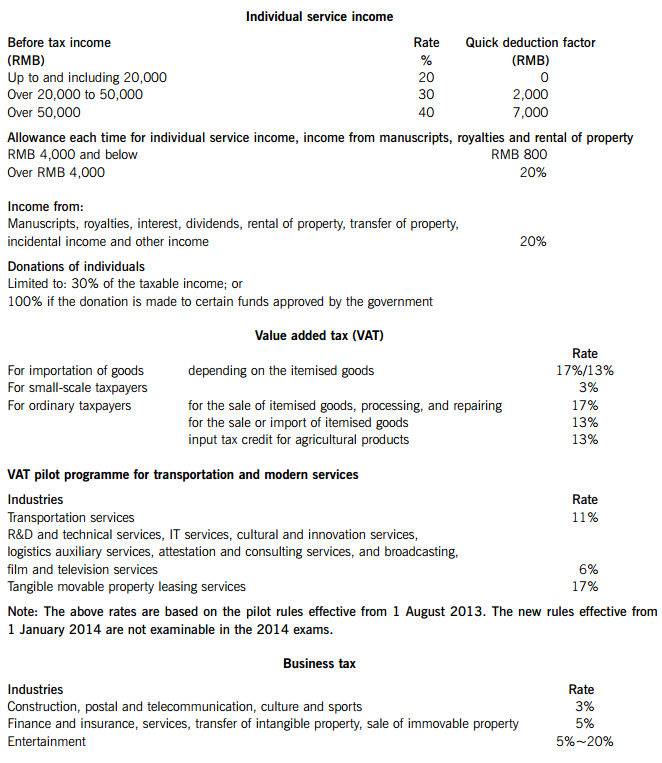

1. Calculations and workings need only be made to the nearest RMB.

2. All apportionments should be made to the nearest month.

3. All workings should be shown.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

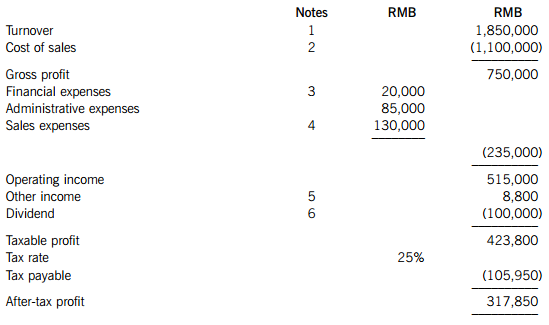

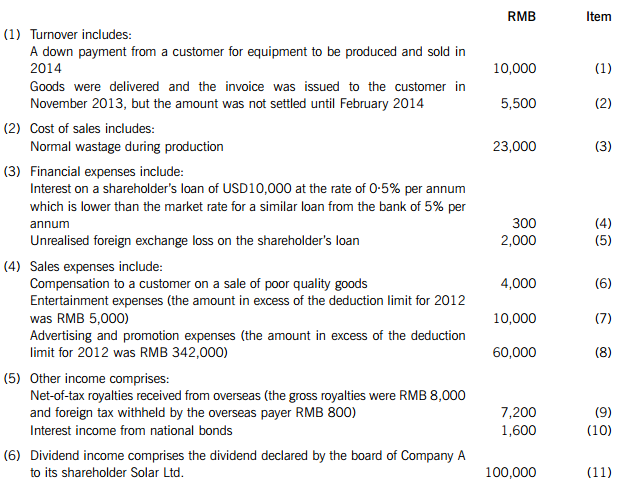

(a) Company A is a foreign investment enterprise set up in China, which manufactures and sells solar power equipment. The only shareholder of Company A is Solar Ltd, a company incorporated in the British Virgin Islands (BVI). The following is a summary of Company A’s income statement for 2013.

Notes:

Required:

(i) Briefly explain the enterprise income tax (EIT) treatment of each of the items identified as (1) to (11). State clearly the items for which no adjustment is required. (13 marks)

(ii) Calculate the correct amount of EIT payable by Company A for the year 2013 starting with the taxable profit of RMB 423,800. (4 marks)

(iii) Calculate the amount of tax to be withheld by Company A from the dividend payable to Solar Ltd. Note: There is no treaty relief between China and the British Virgin Islands (BVI). (1 mark)

(b) An overseas company, P Ltd, provided management services to a China customer for a gross service fee of RMB 100,000. P Ltd is considered as having a China permanent establishment by the tax bureau, which has assessed a deemed profit rate of 50% on the service fee earned by P Ltd.

Required:

(i) Calculate the business tax and enterprise income tax (EIT) payable by P Ltd on the service fee. (3 marks)

(ii) State the circumstances in which the tax authorities can assess the taxable profit of a non-resident enterprise on a deemed basis. (2 marks)

(c) (i) State the FOUR types of tax exempt income for enterprise income tax (EIT) purposes. (4 marks)

(ii) Briefly explain the tax treatment of expenses incurred to earn non-taxable income and tax exempt income. (2 marks)

(d) Company Cap demolished its old factory building and constructed a new one in 2013. The following information relates to these transactions in 2013:

(1) The cost of the old factory building was RMB 400,000 and its net book value as at 1 January 2013 (for both accounting and taxation purposes) was RMB 60,000. The old factory was demolished on 1 January 2013.

(2) Materials were transferred from inventory for the construction of the new factory. The cost of these materials was RMB 90,000 and their selling price was RMB 100,000.

(3) To finance the construction of the new factory, a loan of RMB 500,000 was borrowed from 1 January 2013 at an interest rate of 8% per annum. The loan was repaid on 31 December 2013.

(4) A construction company was engaged to build the new factory with a contract sum of RMB 700,000.

(5) The new factory building was completed on 15 November 2013 and started operations from 16 November 2013.

(6) Company Cap adopted an economic life for the new factory building of 20 years and a residual value of 10%, for both tax and accounting purposes.

Required:

(i) Calculate the cost base of the new factory building for depreciation purposes. (4 marks)

(ii) Calculate the amount of depreciation on the new factory building for 2013. (2 marks)

2.

(a) Mr Chen, a Chinese national, was hired by an IT company in 2012. His employer has proposed the following two alternative remuneration packages both with a total of RMB 300,000 to him for 2013:

Plan 1: A salary of RMB 17,500 each month for 12 months and an annual bonus of RMB 90,000.

Plan 2: A salary of RMB 5,000 each month for 12 months, a special award in June of RMB 120,000 and an annual bonus in December of RMB 120,000.

Required:

Calculate the total individual income tax (IIT) payable by Mr Chen for the year 2013 in respect of each of the two plans.

(b) Ms Li, a Chinese national, earned the following income in 2013.

(1) Coupons for RMB 200 which were given as a result of her bulk buying when she bought groceries from a supermarket for RMB 1,500. She used the coupons to purchase groceries in the next month.

(2) Won a lottery prize of a smart phone with a value of RMB 3,000 from a supermarket. The supermarket has agreed to bear the individual income tax (IIT) payable by the winners.

(3) Received bank deposit interest of RMB 2,000.

(4) Lent Company W RMB 100,000 for a year at an interest rate of 15% per annum.

(5) Wrote a long article for the newspaper, PP Daily, which was published on three days from 1 to 3 February and received a fee of RMB 1,500 for each day.

(6) As the independent non-executive director of a listed company, received a director’s fee of RMB 10,000 each month, i.e. a total of RMB 120,000 for the year.

(7) Received employment income from two separate employments as follows:

– from a retail shop for the period 1 to 15 April, a salary of RMB 2,800; and

– from a restaurant for the period 16 April to 30 April, a salary of RMB 2,500.

Neither the retail shop nor the restaurant withheld any IIT for her.

Required:

Calculate the individual income tax (IIT) payable by Ms Li for 2013 in respect of each of the items of income (1) to (7). State clearly any item(s) which are ‘exempt from IIT’ or ‘not subject to IIT’. (8 marks)

(c) (i) Mr Zhang has a China domicile. In 2013, he was seconded to Hong Kong to work and earned a salary from this Hong Kong employment. After his secondment, he will return to China.

Required: State, giving reasons, whether Mr Zhang will be taxable in China on the salary from his Hong Kong secondment. (2 marks)

(ii) Ms Robin is a model working in the Hong Kong Special Administrative Region. Her Hong Kong employer sent her to China for a fashion show for five days in 2013. She earned a salary from her work at the fashion show. Except for this fashion show, Ms Robin did not spend any time in China in 2013.

Required:

State, giving reasons, whether Ms Robin will be taxable in China in 2013. (2 marks)

(d) Mr Wang is a China tax resident. In 2013, Mr Wang’s only income was employment income of RMB150,000 and his employer withheld the correct amount of individual income tax for him.

Required:

(i) State whether Mr Wang is required to submit an annual individual income tax (IIT) return. (1 mark)

(ii) State the tax filing deadline for the annual IIT return for the year 2013. (1 mark)

3.

(a) Electronic Ltd is a newly set up retail company selling computer accessories. Electronic Ltd’s finance manager prepared the following budget for 2013:

(1) Sales of goods to individual customers at a value added tax (VAT) inclusive price of RMB 780,000.

(2) Purchases of goods from a VAT general taxpayer at a VAT exclusive price of RMB 600,000.

Required:

(i) Calculate the value added tax (VAT) payable by and the gross profit of Electronic Ltd for 2013, if it is a VAT general taxpayer. (3 marks)

(ii) Calculate the VAT payable by and the gross profit of Electronic Ltd for 2013 if it is a small-scale taxpayer. (3 marks)

(b) Clothy Ltd is a factory producing garments for export, it does not have any domestic sales in China. The costs of production of the garments sold by Clothy Ltd in 2013 comprised:

(1) Raw materials of RMB 200,000 purchased for which special value added tax (VAT) invoices were received.

(2) Wages and salaries of RMB 50,000.

(3) Overhead costs for water, electricity, transportation, etc with a total input VAT of RMB 10,000, all of which are supported by valid VAT invoices.

Clothy Ltd had two options for the export of all of the garments produced in 2013:

(i) To export them itself, directly to an overseas customer for a price of RMB 400,000; or

(ii) To sell the garments to a Chinese trading company for a price of RMB 360,000 and the trading company will then export the garments to the overseas customer at a price of RMB 400,000.

The VAT refund rate for garments is 16%.

Required:

(i) Calculate the export value added tax (VAT) refundable to Clothy Ltd for the direct export of the garments. (2 marks)

(ii) Calculate the export VAT refundable to the trading company for the export of the garments purchased from Clothy Ltd. (1 mark)

(c) Toyly Ltd had the following transactions in 2013:

(1) Sold goods for cash-on-delivery in August and the customer paid in September.

(2) Sold goods on credit terms of 30 days after delivery. The goods were delivered in February.

(3) Sent goods on consignment to the consignee in March. The consignee sold the goods in May and passed a statement of the sale to Toyly Ltd also in May.

(4) Sent goods to a branch in another province for sale in November. The branch sold the goods in December.

(5) Received money from Customer X and issued a VAT invoice for the goods in June, but did not deliver the goods until July.

Required:

In the case of each of the transactions (1) to (5), state the month in which Toyly Ltd’s value added tax (VAT) liability will crystallise. (5 marks)

(d) Softko Ltd, a software development company, is a value added tax (VAT) general taxpayer. Softko Ltd had the following transactions in October 2013. All amounts are exclusive of VAT unless stated otherwise.

(1) Paid a software fee of USD2,000 to an overseas supplier. VAT was withheld and paid to the tax bureau.

(2) Purchased ten computers as fixed assets for RMB 100,000. A special VAT invoice was obtained. The computers are used for both taxable and tax exempt services and are used around 20% of the time to provide VAT exempt services.

(3) Paid a software house, which is a small-scale taxpayer, a gross amount of RMB 30,000 inclusive of VAT. A special VAT invoice issued via the tax bureau was obtained.

(4) Hired a coach for transporting its staff from the metro-station to the office for RMB 50,000. A special VAT invoice was obtained.

(5) Acquired a mainframe. computer for RMB 40,000, specifically for the development of some software for an overseas customer. A special VAT invoice was obtained. Softko Ltd has applied for VAT exemption on the export of the software overseas.

Required:

Calculate the input value added tax (VAT) of Softko Ltd for the month of October 2013. Clearly identify any item(s) for which input VAT is not creditable and state the reason. (6 marks)

4.

(a) The following transactions were undertaken by the persons indicated in 2013:

(1) A university set up by the local government received tuition fees of RMB 170,000 from students studying for bachelor degrees.

(2) A property developer sold used computers for RMB 20,000.

(3) A factory received rent of RMB 48,000 from sub-leasing an unused area.

(4) A trading company received bank interest income of RMB 10,000.

(5) A trading company received interest income of RMB 38,000 from lending to another company.

(6) A construction company provided construction services for RMB 500,000.

(7) The government transferred a land use right to a property developer for RMB 26,000,000.

(8) A company used a trademark valued at RMB 320,000 as a capital contribution to another company.

(9) A hotel charged a customer a total fee of RMB 1,300, of which RMB 100 was for the soft drinks from the refrigerator.

(10) A son received a villa valued at RMB 2,000,000 from his father’s estate.

(11) A property management company received a total of RMB 24,000 from tenants, of which RMB 12,000 was for the allocation of electricity and water costs to the tenants and RMB 8,000 was for the salaries of the guards.

Required:

In each of the cases (1) to (11), calculate the business tax payable where relevant, and where not relevant, state clearly whether the transaction is ‘subject to VAT instead of business tax’ or ‘exempt from business tax’ or ‘not subject to business tax’.

Note: Marks will not be given for stating ‘not taxable’. (11 marks)

(b) Cosmet Ltd, produces and sells cosmetics. Currently, Cosmet Ltd makes three standard types of goods with selling prices and costs as follows. All amounts are stated exclusive of value added tax (VAT).

In December 2013, Cosmet Ltd had the following transactions:

(1) Sold 4,200 sets of a pack containing rouge with a lipstick at a price of RMB 100 for each set.

(2) Sold 1,000 sets of hand cream with a lipstick at a price of RMB 50 for each set.

(3) Gave 100 pieces of lipstick to participants during the company’s annual dinner.

(4) Purchased 3,000 pieces of rouge from another factory at RMB 30 each and sold 2,500 of these purchased pieces at the same selling price as for its own rouge of RMB 80 each.

Required:

For each of the transactions (1) to (4), calculate the consumption tax payable by Cosmet Ltd or state clearly if the transaction is ‘not subject to consumption tax’. (4 marks)

5.

(a) State the FIVE methods which the tax authorities can use to carry out a special tax adjustment (transfer pricing adjustment) where a transaction is not conducted at arm’s length. (5 marks)

(b) Company D underpaid its enterprise income tax (EIT) for the year 2012 by RMB 230,000 because it overstated its deductible expenses by using fraudulent invoices for its annual tax filing. The tax bureau discovered the overstatement of expenses and considered it as an act of tax evasion and imposed a penalty on Company D. Company D settled the underpaid tax on 31 July 2013.

Required:

(i) Calculate the amount of late payment surcharge which Company D would have had to pay when it settled the underpaid tax on 31 July 2013. (2 marks)

(ii) State the range of penalties which the tax bureau could have imposed on Company D. (1 mark)

(c) The accountant of Company E wrongly typed income of RMB 10,000 as RMB 100,000 in the company’s tax return for February 2008 and as a result Company E overpaid its business tax by RMB 4,500.

Required:

State, giving reasons, whether Company E can obtain a refund of the business tax overpaid from the tax bureau in 2014. (2 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第3题

Negotiating is the process of communicating back and forth for the purpose of reaching an agreement. It involves persuasion and compromise, but in order to participate in either one, the negotiators must understand the ways in which people are persuaded and how compromise is reached within the culture of the negotiation.

In many international business negotiations abroad, Americans are perceived as wealthy and impersonal. It often appears to the foreign negotiator that the American represents a large multi-million-dollar corporation that can afford to pay the price without bargaining further. The American negotiator's role becomes that of an impersonal supplier of information and cash.

In studies of American negotiators abroad, several traits have been identified that may serve to confirm this stereotypical perception, while undermining the negotiator's position. Two traits in particular that cause cross-cultural misunderst anding are directness and impatience on the part of the American negotiator. Furthermore, American negotiators often insist on realizing short-term goals. Foreign negotiators, on the other hand, may value the relationship established between negotiators and may be willing to invest time in it for long-term benefits. In order to solidify the relationship, they may opt for indirect interactions without regard for the time involved in getting to know the other negotiator.

Clearly, perceptions and differences in values affect the outcomes of negotiations and the success of negotiators. For Americans to play a more effective role in international business negotiations, they must put forth more effort to improve cross-cultural understanding.

(1) What kind of manager is needed in present international business and foreign investment?

A、The man who represents a large multi-million-dollar corporation.

B、The man with knowledge of foreign languages and skills in cross-cultural communication.

C、The man who is wealthy and impersonal.

D、The man who can negotiate with his foreign counterparts.

(2) According to the passage, international business negotiation involves.

A、short-term goals

B、long-term benefits

C、information and cash

D、persuasion and compromise

(3) In the foreign negotiators’eyes their American counterparts are.

A、impersonal suppliers of information and cash

B、skillful in negotiation

C、good at establishing relationship between negotiators

D、indirect and impatient

(4) Which of the following is NOT mentioned in the passage?

A、Foreign negotiators are willing to invest time in relationship between negotiators.

B、American negotiator's directness and impatience cause cross-cultural misunderstanding.

C、Americans has played a more effective role in international business negotiations.

D、Foreign negotiators think that American can afford to pay the price without bargaining

(5) What is the topic of this passage?

A、The differences between American negotiators and foreign negotiators

B、Negotiation skills

C、International business and cross-cultural communication

D、Cross-cultural understanding

第4题

For this part, you are to write an essay on the topic Computer Network in three paragraphs. You are given the first sentence of each paragraph. Your part of the composition should be about 120 words, not including the words given. You should write this composition on the Composition Sheet.

Computer Network

1) Computer networks have enabled us to do a number of things more easily and quickly.

2) However, if not properly dealt with, Internet would bring problems too.

3) Therefore, the safety of networks has increasingly become a public concern.

第5题

Effective adaptation draws upon a number of cognitive processes, such as perception, learning, memory, reasoning, and problem solving. The main trend in defining intelligence, then, is that it is not itself a cognitive or mental process, but rather a selective combination of these processes purposively directed toward effective adaptation to the environment. For examples, the physician noted above learning about a new disease adapts by perceiving material on the disease in medical literature, learning what the material contains, remembering crucial aspects of it that are needed to treat the patient, and then reasoning to solve the problem of how to apply the information to the needs of the patient. Intelligence, in sum, has come to be regarded as not a single ability, but an effective drawing together of many abilities. This has not always been obvious to investigators of the subject, however, and, indeed, much of the history of the field revolves around arguments, regarding the nature and abilities that constitute intelligence.

What does the passage mainly discuss?

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!

微信搜一搜

微信搜一搜

上学吧

微信搜一搜

上学吧

上学吧

微信搜一搜

上学吧